Morning

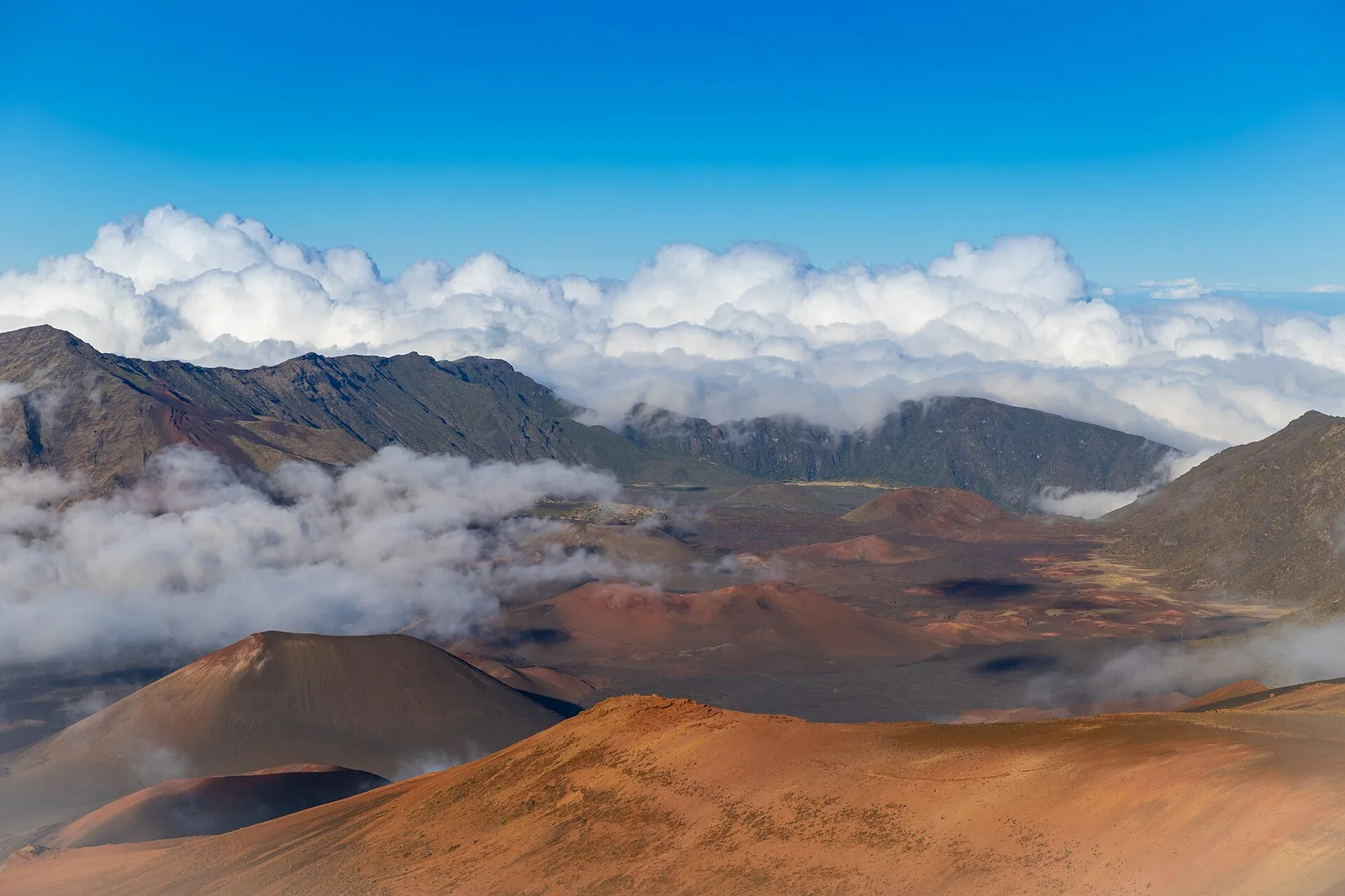

Sunrise at Haleakalā (reservation required)

The national-park permit system is a trap for unprepared guests. A host who pre-books the 3am summit permit for a guest is unforgettable.

Expert short-term rental marketing to grow your bookings and nightly rate in Maui, Hawaii, USA.

* Market averages. Properties marketed by Cavmir typically exceed these figures by 25–45%. Data sourced from AirDNA, STR market reports, and Cavmir internal analytics.

Maui is consistently ranked among the world's top travel destinations — and for good reason. The Valley Isle offers an extraordinary range of landscapes within a short drive: the black sand beaches of Waianapanapa State Park, the sunrise summit of Haleakalā National Park, the lush Road to Hāna, and the luxury resort strips of Kāʻanapali and Wailea. Guests come for once-in-a-lifetime experiences, and they're willing to pay for a property that matches the setting.

Maui's STR market benefits from Hawaii's regulatory framework limiting short-term rentals in certain zones, which concentrates demand on legally-permitted properties. Average nightly rates are among the highest in the United States. Properties in West Maui (Kāʻanapali, Lahaina) and South Maui (Wailea, Kihei) are the most sought-after.

Nearby Markets: Honolulu

A few of the visual fingerprints we lean into when we shoot, brand and market a Maui property — courtesy of the open Wikimedia Commons archive.

In a market where supply is legally constrained and demand remains consistently strong, your biggest challenge is standing out and pricing correctly. Cavmir positions your Maui property for premium guests — through compelling branding, professional drone photography showcasing the island's beauty, and targeted marketing to the high-value traveler segment.

Short-term visitor accommodation in Maui long predates the word 'tourism.' Ancient Hawaiians practiced the aloha tradition of hosting traveling chiefs and guests for extended stays, with reciprocal gift exchange — a cultural memory that still shapes how the best Maui hosts treat guests today. Modern visitor lodging arrived with the steamship era in the late 1800s, exploded after statehood in 1959, and took its present form with the 1960s–1980s development of Kāʻanapali and Wailea as master-planned resort communities. Condominium STRs ('condotels') have been part of the landscape for 40+ years — long before Airbnb existed.

The Airbnb era brought a different kind of STR to Maui: ordinary residential homes and apartment-zoned condos rented to visitors. This collided with Maui's acute housing crisis, which became catastrophic after the August 2023 Lahaina wildfire displaced more than 12,000 residents. That single event reshaped Maui's regulatory posture more than any market force has in a generation.

Maui pricing divides sharply by legal status. Legally permitted STRs — properties on Maui's Minatoya List, in hotel zones, or in grandfathered condominiums — can charge among the highest nightly rates in the United States (Wailea oceanfront routinely clears $900–$2,200 per night). Properties outside those categories face an existential question, not just a pricing question. On the legal side, luxury oceanfront in Wailea and Kāʻanapali commands the premium; Kihei and North Shore properties trade mid-range; up-country Kula and Makawao attract a distinct slower-travel guest willing to pay for cooler air and pastureland views.

The highest-leverage pricing tool for legally operating Maui STRs is minimum-stay policy. Five-to-seven-night minimums (common and often required) filter for the family-vacation guest who spends more per stay, books 4–8 months out, and leaves better reviews than a three-night-weekend guest.

Maui's peak is December 15 through April 15 — snowbird season, spring break, and humpback whale watching. July–August is the family-vacation peak. May, September, and early December are the shoulder windows where dynamic pricing makes the biggest difference. The costliest mistake is pricing shoulder season too low in reaction to fewer inquiries — the actual problem is usually visibility, not price. Lowering rates from $550 to $400 signals a $400 property; lowering minimum nights and investing in paid placement typically recovers occupancy at sustainable rates.

This is the most consequential regulatory story in any US STR market right now. In December 2025, Maui Mayor Richard Bissen signed Bill 9 into law — legislation designed to phase out roughly 6,200 apartment-zoned vacation rentals by January 1, 2029 (West Maui) and January 1, 2031 (South Maui and elsewhere). The legislation passed the County Council 5–3. In February 2026, the Maui Planning Commission voted against a follow-up proposal to create new hotel-zone categories that would have preserved some of the affected units — reinforcing that the phase-out is intended as policy, not negotiating posture.

The units most affected are those on the county's Minatoya List — apartment-zoned condos that have operated as STRs for decades under a 2001 legal interpretation. Properties in true hotel zones (H-1, H-2), on agricultural land with legally permitted B&B permits, or in the specifically designated resort districts are not affected. If you own a Maui STR, step one is determining which category applies to your property — this single question is now worth six figures of lifetime revenue difference. Consult a local attorney who specializes in Maui land use.

If your Maui property is clearly in a legal hotel/resort zone, your strategy is quality and brand differentiation — supply is essentially fixed by law, so better-marketed properties will keep capturing outsized share through the phase-out and beyond. If your property is on the Minatoya List and affected by Bill 9, the urgent questions are: how many years of STR operation remain, what does that do to your amortized investment thesis, and does a sale to a long-term rental buyer or owner-occupant make sense before the phase-out deadline compresses pricing.

Second — embrace longer minimum stays than you think you need. Five-to-seven nights is standard; ten-night minimums in peak season can actually lift annual revenue by capturing the multi-generational family trip segment. Third — respect Hawaiian culture in your listing content. Guests who book Maui are increasingly sensitive to whether a property acknowledges that it sits on occupied indigenous land; listings that address this thoughtfully tend to attract the higher-quality guest.

Three challenges define Maui STR ownership now. First, regulatory risk: whatever your current legal status, the political climate in 2026 favors further restrictions. Second, insurance: wildfire exposure pushed premiums up 30–80% across much of the island after 2023, and some carriers pulled out entirely. Third, tourism politics: 'Don't come to Maui' messaging from community groups has periodically suppressed visitor demand, and responsible hosts need to communicate around — not through — that narrative.

Post-2023-wildfire, Maui insurance is a specialty market. Standard carriers (State Farm, Allstate) have scaled back. Many owners now pair surplus-lines property coverage with STR-specific liability (Proper, CBIZ). Budget $5,000–$15,000 annually for a typical condo, higher for single-family homes. Wildfire mitigation (defensible space, non-combustible roofing) increasingly affects insurability, not just premium.

Hawaii property tax on STRs is aggressive — Maui's 'TVR-STRH' property-tax classification carries substantially higher rates than owner-occupied (roughly $11.85 per $1,000 assessed as of 2025, vs. $2.00 for owner-occupied). This is by design: the county uses property-tax differential as an STR discouragement tool. Budget carefully. GET (4.712%) and TAT (13.25% combined) are collected from guests but are the owner's legal responsibility to remit.

Hawaii conforming loan limits are elevated (ZIP-code specific), which helps. STR-specific DSCR loans are available but typically carry rate premiums and require proven rental history — increasingly difficult for new Maui STRs given regulatory uncertainty. Several national lenders have restricted new Maui STR underwriting post-Bill 9. Expect 20–30% down minimum and to qualify more on liquid reserves than on projected income.

Maui in 2027 will look measurably different from Maui in 2024. Bill 9 enforcement ramps through 2028 (West Maui) and 2030 (South Maui), meaning remaining legal inventory will become scarcer and more valuable. Expect average rates on legally operating STRs to rise materially through 2028. Watch for follow-up legislation — the 2026 Planning Commission vote against hotel-zone workarounds suggests the political appetite for restriction has not peaked. Properties in designated hotel zones, legitimate B&Bs on agricultural land, and purpose-built resort condos are the three categories most insulated from further change.

If Bill 9 affects your Maui property and you're exploring markets with less regulatory tightening, properties in the Turks and Caicos, the Dominican Republic, and Tulum deliver tropical-premium positioning with lighter STR-specific restrictions. Cavmir works in all three.

Maui is one of those places that resists ordinary marketing. You can't photograph it the way you photograph a beach resort — the island is too theatrical for that. Waianapanapa's black sand with the ocean slamming the lava cliffs, the banyan in Lahaina, Haleakalā at dawn where the light comes up out of the crater, the ribbon of Road to Hāna falling through six waterfalls in twenty minutes — every location has a signature frame most listings fail to capture because they shoot the house, not the island around it.

The regulatory tightening on Maui since 2023 changed the marketing calculus entirely. A legally-permitted STR here is now a scarce asset, which means the question is no longer "how do we get bookings" — it's "how do we attract the right bookings at the right rate." We love Maui because it's a market where brand genuinely matters. Guests book Maui six months out; they're researching, comparing, saving to Pinterest boards. A property with an editorial brand, authentic Hawaiian storytelling, and drone footage of the surrounding coastline wins those guests at a rate premium that no amount of platform optimisation can replicate. The properties that still win here are the ones that treat themselves as small hospitality brands — not listings.

The picks Cavmir recommends for Maui welcome books — the details guests repeat to friends back home and that make a review glow.

The national-park permit system is a trap for unprepared guests. A host who pre-books the 3am summit permit for a guest is unforgettable.

South-shore sunset over the Kaho'olawe silhouette. Less crowded than Wailea, and the photos read dramatic without the resort furniture in frame.

The old sugar town with surf-shop character and a coffee culture older than the condos. Walkable in an hour, photographable in fifteen minutes.

The one Maui reservation that runs out first. A welcome book that flags the lead time is a welcome book that gets forwarded to the guest's friend.

Upcountry bakery, cash only, sell out by 9am. The kind of detail that turns a rental into a vacation story.

Pre-summer shoulder fills up if marketed to the festival calendar — a window most hosts ignore and most platforms under-price.

Half-day round trip to an island that feels like private Hawai'i. Cruise guests skip it; STR guests have the time to go.

Hawai'i banned oxybenzone sunscreen in 2021. Guests arrive with the wrong bottle. A host who stocks mineral sunscreen saves a beach day.

Composite engagements representative of Cavmir's Maui work. Property identifiers removed, figures anchored to public AirDNA ranges and our own post-campaign analytics.

Generic listing in a building with 40+ competing units. ADR was tracking $80 below building median; occupancy 61% against a market benchmark of 76%. Photography was agent-grade, not editorial.

We differentiated by context rather than amenity. Full re-shoot at dawn with drone coverage of the North Beach coastline, interior restyled in a quiet Hawaiian palette that contrasted with the building's beige baseline. Rewrote copy around quiet mornings, family-oriented snorkel culture, and whale-watching season. Built a direct-booking site with a three-night-minimum structure that protected the premium-guest segment.

Occupancy moved to 82%. ADR climbed 34% and held through an entire soft season. Whale-season pricing (Dec–Apr) cleared a 1.9× multiplier over prior-year performance.

Ultra-premium home competing with resort suites. Guest profile needed a polished brand narrative — not a listing. Owner had historically relied on word-of-mouth and a single travel agent.

Cavmir built a full brand system: custom logomark, editorial brand book, cinematic property film, and a short-form content library spanning the home's signature moments. Distribution expanded to luxury-travel advisors (Virtuoso network), two concierge-tier direct-booking platforms, and curated Pinterest boards. Pricing was restructured around a floor-rate model tied to the shoulder/peak/gala calendar rather than platform averages.

First full year revenue up 47%. Advisor-channel bookings now represent 34% of revenue and book 4–6 months ahead, smoothing the revenue curve. Peak-week ADR holding at $2,890.

Off-beach property struggling to compete with coastal listings. Owner wanted to position as an alternative to resort culture, but copy and photography kept defaulting to apology — "only 30 minutes to the beach."

We inverted the frame. Rewrote the listing as a destination in its own right: upcountry quiet, the Maui locals prefer, cool nights, working-farm aesthetics, the paniolo (Hawaiian cowboy) culture. Photography leaned into jacaranda season and the eucalyptus groves. Distribution targeted repeat Hawaii visitors who'd already "done" the beach on previous trips.

Occupancy climbed from 58% to 74%. Guest profile shifted measurably toward repeat Hawaii travellers, longer average stay (6.2 nights vs 4.1), and a 4.9-star review average from a more intentional guest. ADR up 19% year-over-year.

Demand in Maui peaks around January, February and June and runs quietest around September through October. Here is how the year actually books — and what to do about each stretch of the calendar.

Maui's big season is mid-December through March, when whale season, holiday travel and winter escapes stack together and well-run listings hold firm rates for weeks at a time. June and July bring a second peak of families. Have the calendar priced and the listing polished by early fall for winter and by late winter for summer — the strongest dates go to hosts who were ready first.

April, May and late fall are the in-between months, carried by couples, honeymooners and travelers who deliberately avoid the crowds. November builds toward Thanksgiving week, when the Maui Invitational and holiday travel firm up West Maui dates. The shoulder play is flexibility: shorter minimums, midweek-friendly pricing and copy that leans into calmer beaches and easier restaurant tables.

September and October are the honest lull once families go back to school. Long-stay travelers and late-deciding couples keep things moving if your minimums and pricing let them, and it's the right window for deep cleaning, photo refreshes and listing rewrites before whale season. Resist slashing rates across the board — targeted midweek flexibility does the same job with less damage.

Whale season and the winter holidays book many months ahead, and repeat winter guests often rebook next year on their way out the door. Summer families commit by early spring. September and October run on a short fuse, with couples booking weeks or days out — keep pricing responsive even when the calendar looks thin.

Most Maui trips run five nights to a week or more — nobody crosses the Pacific for a weekend. Winter long-stayers stretch to two weeks or a month, especially in South Maui condos, while summer families cluster tightly around the school-break weeks.

The Maui winner is a turnkey condo in a well-known complex along the Kihei, Wailea, Kaanapali or Napili coastline, with an ocean view the photos can prove. Inside a big complex you're competing against near-identical floor plans, so presentation is the whole game: better photography, sharper copy and a rate strategy tuned to whale season separate you from the stack. Ground-floor units win families; top-floor views win couples.

Lead with proof of the view and the light — Maui guests compare dozens of near-identical condos, and honest, beautiful photography of your actual unit is the fastest separator. Write the listing around your area's story: whale season off the south and west shores, snorkel mornings in Kihei and Wailea, sunsets on the Kaanapali side. Then capture the repeat-guest economics with a direct-booking site and an email list, because Maui visitors come back on a schedule. That's the layer a marketing agency like Cavmir adds — photography direction, listing copy, direct booking and search visibility working as one system.

Mid-December through March is the heart of it, when whale season and winter escapes overlap and the holiday weeks become the most valuable dates of the year. June and July bring a second family-driven peak. September and October are the quietest months, with spring and late fall as workable shoulders.

Whale-season and holiday stays book many months out, and repeat winter guests often lock in the following year before they leave. Summer families commit by early spring. The fall lull is short-notice territory, so the practical rhythm is: winter dialed by early fall, summer dialed by late winter, and responsive pricing in between.

West Coast nonstops into Kahului carry the bulk — Los Angeles, the Bay Area and Seattle above all — joined by heavy Canadian traffic in winter and Japanese visitors connecting through Honolulu. Phoenix and the mountain states add a steady stream. Inter-island weekenders from Oahu round it out, booking short and late.

An ocean view you can prove in photos is worth more than any single upgrade, followed by air conditioning, which still isn't universal in older South Maui complexes. Beach gear, a lanai set up for dinner outside and pool access decide family bookings, while fast wifi and a workspace hold the long-stay winter crowd. Stock the kitchen properly — week-long guests cook.

Talk to Cavmir today. We'll show you exactly what your Maui property is leaving on the table — and how fast we can change that.

Book a Free Strategy Call